Under periodic inventory systems, only the sales return is recognized, but not the inventory condition entry. In a perpetual weighted average calculation, the company keeps a running tally of the purchases, sales and unit costs. The software recalculates the unit cost after every purchase, showing the current balance of units in stock and the average of their prices. See the same activities from the FIFO and LIFO cards above in the weighted average card below. Periodic system examples include accounting for beginning inventory and all purchases made during the period as credits. Companies do not record their unique sales during the period to debit but rather perform a physical count at the end and from this reconcile their accounts.

5: Basic Merchandising Transactions (periodic inventory system)

- We hope our guide was helpful in understanding the basics of the periodic inventory system.

- Products in the ending inventory are the ones the company purchased most recently and at the most recent price.

- Through point-of-sale inventory systems, the perpetual inventory system keeps track of inventory by immediately documenting any alterations.

- This method is often used by small businesses and those with low-volume sales as it is easier and more cost-effective to implement than a perpetual inventory system.

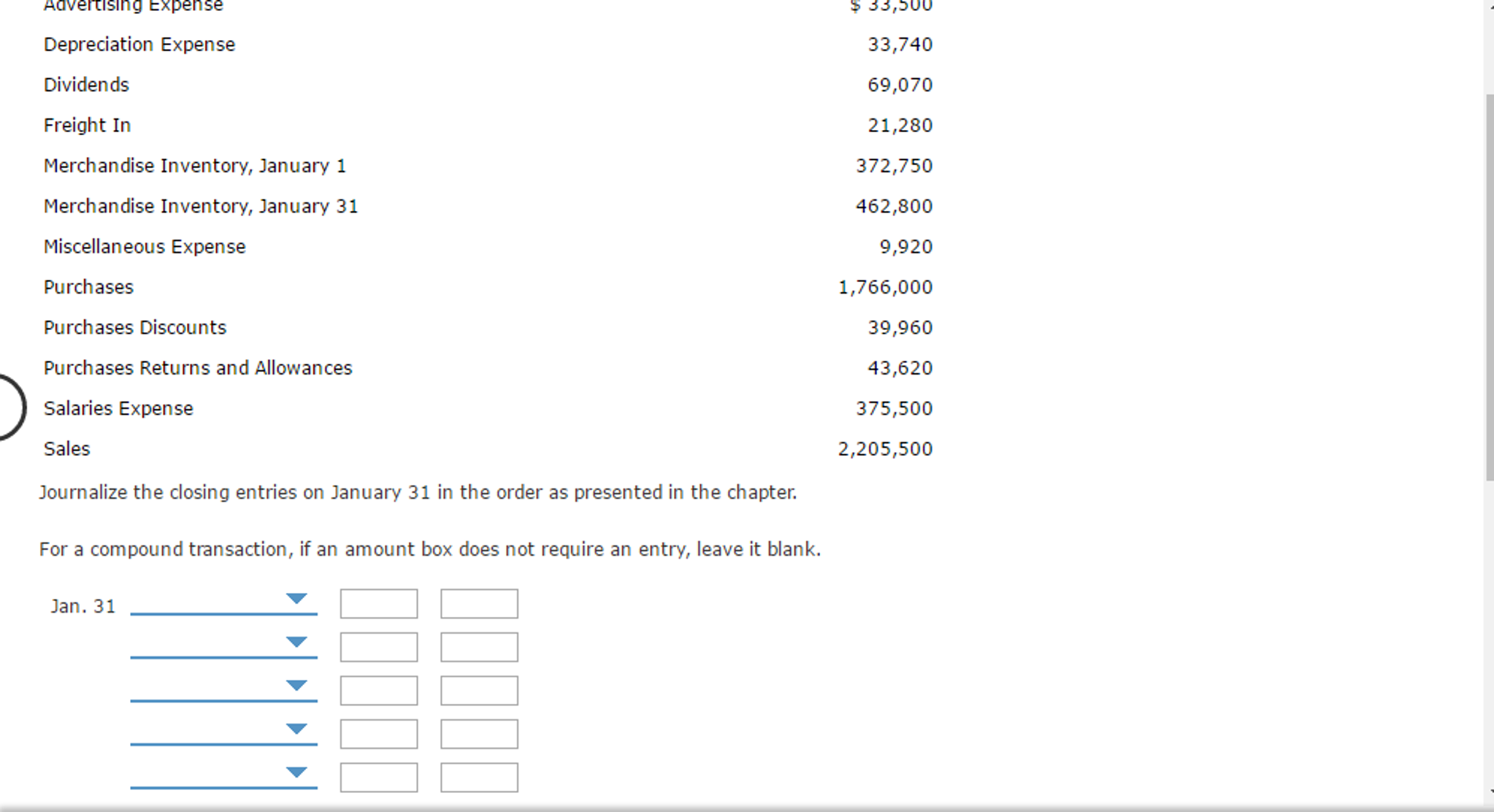

This count and verification typically occur at the end of the annual accounting period, which is often on December 31 of the year. The Merchandise Inventory account balance is reported on the balance sheet while the Purchases account is reported on the Income Statement when using the periodic inventory method. The Cost of Goods Sold is reported on the Income Statement under the perpetual inventory method. A periodic inventory system is a type of inventory control system that relies on physical inventory counts at predetermined intervals to track inventory levels and values.

Periodic FIFO

Read on for a list of the benefits and downsides of the periodic inventory method. So there’s no longer a need for businesses to manually count their merchandise, or write down journal entries by hand. Want to learn more about journal entries and how learn bookkeping and accounting online for free to record them for your small business? Head over to our guide on debit and credit entries, with practical examples. When dealing with a periodic inventory, you’ll likely find yourself journalizing transactions, especially at the end of the year.

Perpetual vs Periodic Inventory System

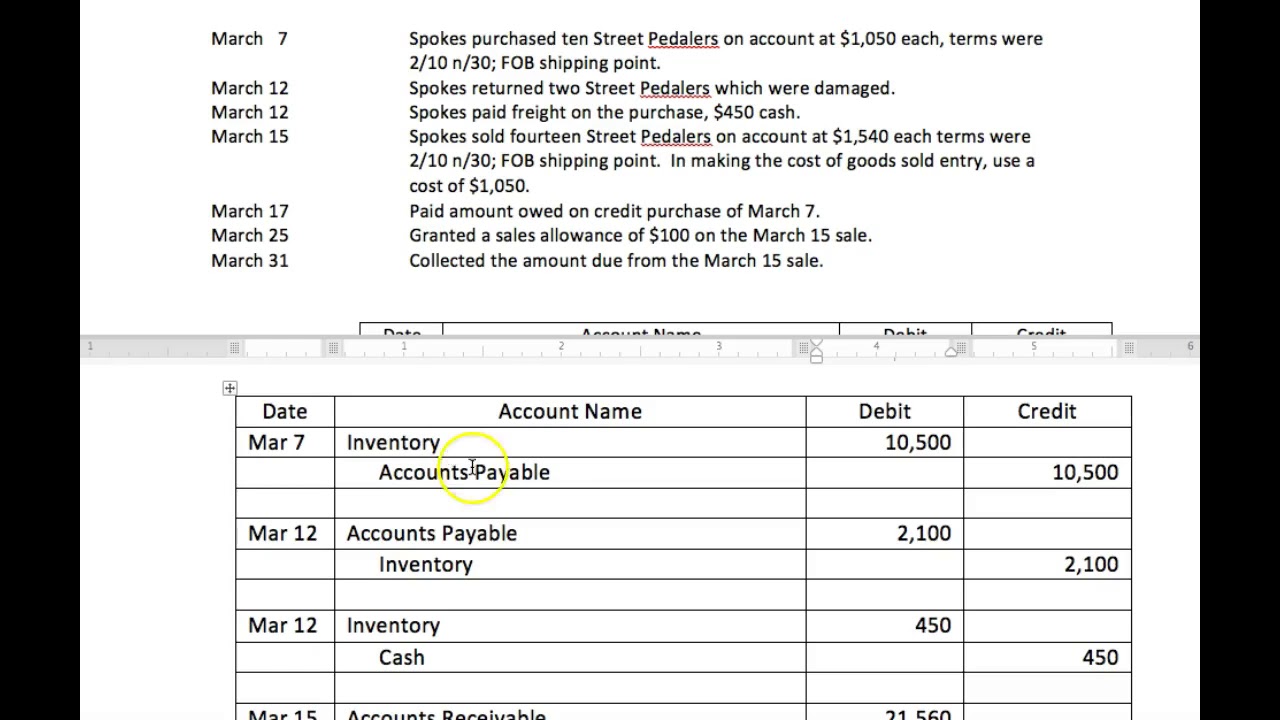

When the stock is counted, the periodic inventory system is used to compare the physical count to the amount that was in the records. The adjusting entry is based on the formula to calculate the cost of goods sold. Thus, the purchases and merchandise inventory (beginning) are added together and represent goods available for sale. Therefore, before any adjusting entries, the balance in the merchandise inventory account will reflect the amount of inventory at the beginning of the year, as indicated in the following T-accounts. The transaction will record inventory based on the month-end physical count. At the same time, we need to reverse last month’s inventory balance otherwise it will double count.

The overall cost of the inventory item is not readily available and the quantity (except by visual inspection) is unknown. At any point in time, company officials do have access to the amounts spent for each of the individual costs (such as transportation and assembly) for monitoring purposes. A periodic inventory system is a type of inventory valuation used at the end of the accounting period by small businesses & early-stage start-ups because of lesser stock in their inventory.

However, larger and expanding companies often choose a permanent inventory system, which is best managed by an ERP inventory module since they require more comprehensive inventory management. Many small firms, especially those with few unique SKUs to update at the end of each quarter, do just fine with periodic inventory, even if it does not provide business decision-makers with real-time data. Record the total accounts payable purchase and accompanying discount in an entry together that debits the accounts payable and credits the purchase discounts account.

This is why effective and efficient inventory management is essential for small businesses and large companies alike. Overall, this system is favored by businesses that don’t require instant stock updates and can manage with periodic counts to keep things simple and cost-effective. In short, while the periodic inventory system may work well for smaller, low-volume businesses, it can be problematic for companies needing tight inventory control and real-time data. At the same time, it prevents a business from planning and forecasting future inventory levels.

The Periodic Inventory System is a straightforward, cost-effective method for managing inventory, particularly for small businesses or those with low sales volumes. While it offers simplicity and reduced administrative burden, it also comes with challenges such as the lack of real-time data and the need for time-consuming physical counts. By understanding its key features, advantages, and limitations, businesses can determine if this system fits their operational needs. Whether you’re a small retailer or a seasonal business, the periodic inventory system provides an easy way to manage stock without the complexities of constant tracking. A periodic inventory system can help businesses stay organized with minimal effort and cost.